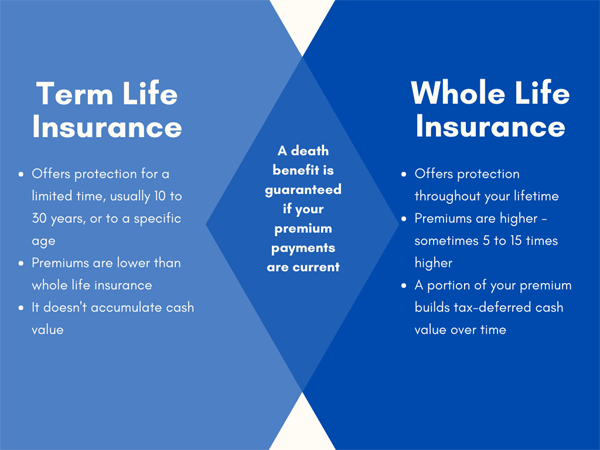

Debunking Common Myths About Whole Life Insurance

Whole life insurance is often surrounded by misconceptions that deter individuals from exploring its benefits. One common myth is that whole life insurance is only for the wealthy. This is not true; while it is generally more expensive than term life insurance, it provides lifelong coverage and a cash value component that can be beneficial for individuals of various financial backgrounds. Additionally, many believe that whole life insurance does not offer a return on investment. In reality, the cash value accumulates at a guaranteed rate, providing both a death benefit and an opportunity to borrow against the policy's cash value.

Another prevalent myth is that whole life insurance is too complex to understand. While it does come with various features, the fundamental principle is quite straightforward: you pay premiums, and in return, your beneficiaries receive a death benefit upon your passing. It's essential to educate yourself on how the policy works, including its dividends, cash value growth, and how it compares with other types of life insurance. Speaking with a knowledgeable insurance agent can help clarify these aspects and dispel any misconceptions you may have about whole life insurance.

The Truth Behind Whole Life Insurance: What You Really Need to Know

Whole life insurance is often touted as a stable and reliable financial product, offering lifelong coverage and a savings component that grows over time. However, many potential policyholders are unaware of the complexities and potential drawbacks associated with it. First and foremost, the premiums for whole life insurance are significantly higher than those for term life insurance, which can lead to budget strain. Moreover, the return on investment is often criticized; policyholders may find that the cash value accumulation is slow and does not keep pace with inflation over the years.

Another important aspect to consider is that whole life insurance typically comes with a variety of fees and costs that can eat into the cash value. This can result in less flexibility when withdraws or loans against the policy are needed. Additionally, the emotional appeal of leaving a financial legacy can cloud the judgment of many buyers, leading them to overlook alternative strategies that might better serve their needs. Ultimately, understanding the full scope of whole life insurance is crucial in making an informed decision, as it may not always be the ideal solution for every financial situation.

Is Whole Life Insurance Worth It? A Deep Dive into Its Benefits and Drawbacks

Whole life insurance is often touted as a financial tool that provides both coverage and a cash value component. One of the primary benefits of this type of insurance is that it offers lifelong protection, meaning your beneficiaries will receive a death benefit regardless of when you pass away, as long as premiums are paid. Additionally, the cash value accumulates over time, and you can borrow against it or withdraw funds when needed, providing a sense of financial security and flexibility. Whole life policies also typically offer guaranteed premiums and cash value growth, adding a layer of predictability to your financial planning.

However, there are notable drawbacks to consider when weighing whether whole life insurance is worth it for you. Firstly, the premiums are significantly higher than those of term life insurance, which can strain your budget in the long run. Furthermore, the cash value accumulation is relatively slow in the initial years, which may not align with your short-term financial goals. It's also important to recognize that if you decide to cancel the policy, you may receive less than you paid in premiums. Therefore, it is crucial to conduct a thorough analysis of your financial situation and future needs before committing to a whole life insurance plan.